At its September 11, 2020 meeting, the Governing Board established the Financial Planning and Procedures Committee (FPPC) to expand the roles of the Investment Committee. The purpose of the FPPC is to work with AFS staff, the Audit Committee, and the AFS Investment Advisor to assess AFS’ current and future financial positions and guide AFS leadership on such matters. The FPPC duties include the following: (1) engage with AFS staff, the AFS Investment Advisor, and others to provide review, recommendations, and evaluation of AFS finances; (2) develop training for the Management Committee to ensure that members understand and better execute the fiduciary responsibilities; (3) develop more transparent tools for reporting on AFS finances to AFS leadership; (4) help AFS staff assess financial reports; (5) facilitate financial assessments of AFS programs; (6) review new program proposals and strategic plans; and (7) revise the AFS Rules and Procedures, as appropriate. Because of its greatly expanded role, the FPPC has fundamentally expanded both the AFS Rules and Procedures documents pertaining to the FPPC. The revised procedures include four major sections: Definitions, Program Planning, Financial Policies, and Investment Objectives and Guidelines.

Definitions

The following definitions are provided for terms that are used throughout this document. Definitions may be further defined where they are presented in the document.

Bank line of credit and collateral account: The American Fisheries Society has a short-term line of credit negotiated with M&T Bank that is available if short-term funding is needed to support AFS operations. As of June 2021, the available credit line was $500,000. It is secured by a collateral account, a second investment account managed by the AFS Investment Advisor. The required collateral is currently $570,000 and is comprised of the same mix of securities as in the investment fund.

Capital budget: The capital budget is the Society’s “infrastructure” plan for long-term assets, such as the Society’s website, member database, and planning tools. The costs to create and manage these assets may be amortized over the useful life of the asset.

Fixed assets: Fixed assets include current fixed assets (office condo, leasehold improvements, and equipment) and the related borrowing and lease purchases, all included in this Procedures manual for purposes of policy and management. Responsibility for management of the fixed assets is delegated to the Executive Director.

Investment advisor: The investment advisor is a paid individual or firm, professionally qualified and licensed to offer financial guidance and trade securities. Typically, this individual or firm is compensated through a management fee as a percentage of account assets.

Investment fund: An investment portfolio managed by a professional investment advisor and reviewed quarterly by the FPPC. The investment portfolio consists of an obligated reserve, unrestricted funds, and restricted funds.

Obligated reserve: The portion of the investment fund equivalent to the 1-year operating budget based on the average operating expense budget over the previous 4 years, adjusted for guaranteed, long-term contractual revenues. The obligated reserve will be maintained as restricted funds within the investment fund.

Operating budget: The operating budget is the Society’s financial plan for the coming calendar year. The operating budget reflects anticipated income and expenses associated with Society programs, investments, and other expenditures to support Society members.

Overhead rate: The annually calculated AFS overhead rate, approved by the U.S. Government, is used to estimate the value of the Society’s administration costs for managing programs and grants.

Restricted funds: Invested funds owned by AFS units (including Chapters, Divisions, and Sections) and endowment funds. Restricted fund monies are managed as part of the investment fund, but the monies are not accessible to support the AFS operating budget.

Short-term money: Includes all cash, cash management accounts, and receivables. These are expected to equal or slightly exceed current liabilities plus anticipated needs for cash over 3–4 months.

Special project: A new project proposed by AFS members that is not already approved within the operating budget.

Unrestricted funds: Invested funds owned by AFS that are not restricted by fund management requirements. Presently, the value of unrestricted funds are those funds in the investment fund that exceed the obligated reserve value.

The American Fisheries Society has four major sources of revenue: membership dues, annual meeting net profits, grants and project management, and publications (including journals and books). The American Fisheries Society has eight major expenditure categories, including staff salaries and benefits, administration, membership, meetings, policy and communications, grants and project management, professional development and awards, and publications. The American Fisheries Society must quantify past trends and estimate future financial trends and then respond accordingly to ensure long-term financial stability while meeting member needs and organization goals.

Budgeting, Program Planning, and Evaluation

The American Fisheries Society supports many programs that provide benefits to Society members. Whereas some programs generate revenue, other programs cost more to maintain than the revenue the programs generate. The American Fisheries Society and the FPPC will institute the following guidelines:

The Executive Director (ED) shall create a list of all programs and activities for budget tracking and expense allocations. The ED shall provide the program list to the FPPC during the annual development of the AFS operating budget. This information shall be summarized in an Excel spreadsheet that AFS shall maintain on the FPPC’s Google drive.

Every three years, the FPPC shall evaluate one-third of the programs and work with the associated AFS committee, if any, to assess financial performance relative to the program’s goals. The FPPC shall provide narrative comments regarding the programs’ performances.

The ED shall maintain an inventory of programs and corresponding financial results and provide them to the FPPC and Management Committee. The Management Committee and the FPPC shall make recommendations to the ED on budget trends and adjustments to meet financial targets. The ED shall act on those recommendations or explain in writing why they cannot do so.

New Program/Service Business Plans

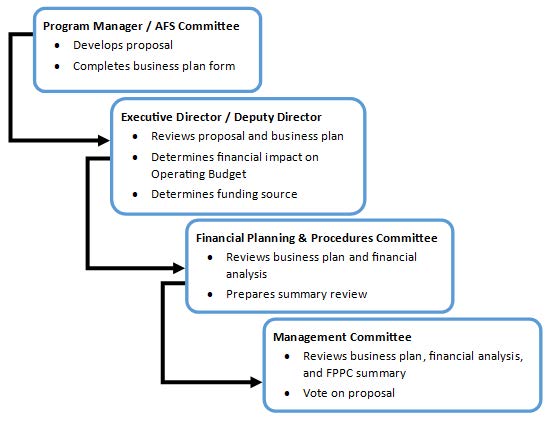

American Fisheries Society members and committees periodically propose new programs and services that must be overseen by AFS staff. New programs require additional staff time and expenses, thereby affecting the operating budget. Proponents propose new programs and services during the annual operating budget development process (as opposed to the below Special Projects process).

The FPPC shall evaluate the financial components, business rationale, and resource allocation for each proposed new program and make recommendations to the Management Committee on the reasonableness of the assumptions and the likely financial impact of the new program on the Society’s operating budget.

The FPPC shall develop a business plan form for assessing the financial and operating elements of the new program. The business plan form shall be completed by the new program proponent and submitted to the ED. The ED shall review the business form and provide a review of anticipated effects to existing staff capacity, non-personnel expenses, and the annual operating budget. The ED shall provide the review report to the FPPC, which shall comment on the review report. The FPPC review report and comments shall accompany the business plan form and program proposal when motioned to the Management Committee for consideration.

Capital Budgeting

The ED shall prepare a three-year capital budget and replacement reserves schedule identifying anticipated financial outlays for major expenditures for the Society’s database, website, and similar significant investments of capital for replacing or acquiring assets.

Program-Planning Decision-Making Process

The following section includes the ideal budget and resource-allocation decision-making process from initial program proposal to the Management Committee’s vote on the proposal.

Financial Reporting

Timely, clear, and concise financial reporting is imperative for presenting AFS financial information to the Management Committee and AFS staff, committees, and members. American Fisheries Society financial reporting includes monthly updates, quarterly reviews, and an annual audit report. Reporting shall include techniques that plainly present financial results for the current period as well as for at least a four-year period to capture financial trends. Terms shall be defined, and anomalous results shall be clearly explained. The FPPC and the ED shall prepare a financial reporting template for Management Committee meetings. A complementary Excel workbook shall also be developed to efficiently update financial results. Working from templates should provide an efficient and repeatable means for reporting financial results. Reported information should increase in detail and breadth from monthly to the annual audit report.

Financial Policies

The following sections provide a review of the Society’s operating budget and investment fund.

Operating Budget

The operating budget is the Society’s financial plan for the coming calendar year. The operating budget reflects the anticipated income and expenses associated with the Society’s programs, investments, and other expenditures. The Society’s financial objectives include managing and providing resources to meet current and future member needs, organization goals, and, at a minimum, maintaining a balanced calendar-year budget.

The annual operating budget is not only based on anticipated revenues and expenses for the coming year, but also compared to the preceding four-year averages of revenues and expenses. The preceding four years of revenues and expenses capture a range of economic and market conditions that affect the Society’s finances. Additionally, a four-year period includes one rotation of the AFS Annual Meeting through each of the four Divisions. Because Annual Meeting net income varies across the four Divisions and Annual Meeting net income is an important revenue item in the operating budget, the four-year average is a moderately conservative approach to predicting this important revenue item.

The Management Committee and the FPPC shall maintain a legacy document that explains the origin of new programs that have a financial impact on the Society’s finances. The legacy document should include a program’s initiation date, the purpose and term of the program, and the expected annual and long-term revenues and expenses associated with the program. It is imperative that the Management Committee assess the cost and benefits of each new program, especially in the context of the operating budget and the Society’s existing obligations.

The annual operating budget shall be presented to the Management Committee and the FPPC for review and approval during the preceding year’s Annual Meeting. Modifications to the operating budget based on more recent data or concerns may be presented to the Management Committee and the FPPC for review and approval in subsequent meetings. If expenditures exceed revenues for one or more years, the FPPC shall engage the Management Committee and ED to review revenues and expenditures and evaluate the implications on programs and the operating budget. The Management Committee is responsible for ensuring that rigorous financial planning is implemented by the ED.

The cost of AFS products and services should, in aggregate, be covered by the revenues accrued from these products and services. Because some AFS products and services do not generate revenue, other programs and services must do so to support the operating budget.

Special Projects

Special projects are proposed after the operating budget has been approved by the Management Committee. Special projects must contribute to the Society’s major goals, and funding sources must be included with the proposal. The following guidelines are to be observed when considering special projects.

The Society shall charge the overhead rate covering headquarters’ costs to all funding proposals except when the granting entity has an explicit policy to prohibit paying overhead (in which case, AFS shall assess whether direct administrative costs can be included, if the Society wishes to absorb those costs, or if the proposal should be abandoned).

Special funding can be sought both to expand current approved activities and to initiate new approved activities. Pass-through projects handled on behalf of AFS units or external parties shall include at least an agreed-upon overhead cost.

Any single project, with projected expenses exceeding $100,000 must have Management Committee approval. No project shall be undertaken until a written business plan is approved by the ED and the Management Committee.

The business plan shall include the project’s purpose, strategy, location(s), management team, funding sources, year initiated, and duration.

There shall be at least an annual update on special project finances. This report shall be part of the ED’s report to the FPPC and Management Committee.

Financial Relationships with Units

The American Fisheries Society is legally responsible for unit obligations. The Society is currently developing a memorandum of understanding that will outline unit responsibilities for maintaining financial standing. The following core policies will apply to units’ financial management:

Unit secretary-treasurers shall send annual financial reports to the ED within 30 days following the unit’s annual business meeting.

All units are required to file an IRS return (Form 990), with a copy sent to the ED.

Checks issued by AFS shall be cashed by units as soon as possible. If the check is not cashed within 180 days, AFS will stop payment.

Chapters shall submit an affiliate member list to AFS by August 1 in order to receive its prior year’s dues rebate.

Fundraising and Development

The American Fisheries Society has experienced flattened or declining revenues associated with membership dues, publication fees, and Annual Meeting net income. The Society is expanding its services, such as meeting planning, to other professional organizations to create additional revenue streams for AFS while assisting other like-minded organizations. The Society should continue to expand revenue opportunities to diversify revenue streams and support the operating budget and investment fund. The AFS Development Manager should be encouraged to pursue relationships with foundations, commercial businesses, and other potential partners. The Society should consider reactivating the Development Committee to support the AFS Development Manager.

Financial Sustainability and Financial Pitfalls

There are numerous financial pitfalls that could impact the Society’s solvency. These pitfalls include both external and internal concerns. Although AFS cannot control external concerns, AFS management must be able to react to them as well as internal shortfalls that affect the Society’s financial condition. Appropriate planning, timely financial reporting and review, and expeditious response is necessary to ensure the Society’s long-term financial sustainability. The following strategies should be employed to avoid financial pitfalls.

Maintain core competency and avoid mission fragmentation: The American Fisheries Society must hold completely to its defined core mission to preserve and enhance its impact. The more effective AFS becomes, the greater the pressure to become engaged with activities that are peripheral to the core mission. The Society should continually evaluate new initiatives to determine their appropriateness in meeting the AFS mission as well as the financial burden new initiatives place on AFS finances.

Fund and maintain the obligated reserve: The obligated reserve should be funded and maintained to provide AFS with a financial buffer and recurring revenue source. Our goal is to meet the obligated reserve target over a seven-year period beginning in 2022 and with annual contributions at the discretion of the Management Committee.

Strategic plans: Developing strategic plans with actionable goals must include coordinating programs and finances to ensure financial sustainability. Funding sources must be identified for new programs or existing programs should be terminated to ensure that enough funding is available in the operating budget. Monitoring progress against operational and financial goals is an important component for ensuring that AFS is functioning effectively and following the strategic plan.

Staffing and staff accountability: Staffing levels and their associated expenses shall be supported by the operating budget. Like new programs, new staff need to be supported by the operating budget. Staff must account for their time and expenses and accurately assign their time and expenses to appropriate project or administrative codes in the AFS accounting software.

Program review: The ED and Management Committee shall annually review programs to determine if programs are supporting the AFS mission and how the programs are affecting AFS finances. Ineffective or expensive programs that do not sufficiently support the AFS mission shall be discontinued.

The following section reviews the AFS investment fund and investment policies.

Investment Fund

The American Fisheries Society has maintained an investment fund with AXA Advisors (name changed to Equitable Advisors) since 2006. Gretchen Bolton, the AFS Investment Advisor, has managed the account since it was established. The investment fund is composed of diversified investments and the account is managed with a moderately aggressive investment objective to provide long-term growth with below-average risk.

The investment fund currently includes the investment fund and the collateral account. Although the collateral account is maintained as a separate account in support of the AFS line of credit, the investment fund and the collateral account have similar investments and the accounts are nearly managed as a singular account.

The investment fund currently includes monies contributed by AFS as well as AFS units and programs. Monies that AFS can freely access are referred to as unrestricted funds; monies that AFS cannot freely access are referred to as restricted funds, which AFS oversees for AFS units and programs. There are three components to the investment fund: obligated reserve, unrestricted funds, and restricted funds. The following sections provide additional detail on these components.

Obligated Reserve

The obligated reserve is a component of the unrestricted funds within the investment fund. The goal for the obligated reserve is to increase the obligated reserve’s value until it is equal to a one-year operating budget, which is based on the average operating budget over the preceding four years. The obligated reserve provides AFS with a financial buffer and serves as a source of stable investment income into the future. Because AFS has drawn down the unrestricted funds portion of the investment fund to support new and existing programs over the past five years, rebuilding the unrestricted funds to achieve the obligated reserve goal may take 5 years. After the obligated reserve achieves a value equivalent to a 1-year operating budget, the spending policy for the obligated reserve shall be based on the accumulation of dividends, interest, redemptions, or realized gains (in sum, the obligated reserve’s annual income) that generate capital exceeding the 1-year operating budget. Target payouts from the obligated reserve shall be up to 50% of the obligated reserve’s annual income at the end of the calendar year. The remaining 50% of the obligated reserve’s appreciation shall remain in the investment fund. Once the obligated reserve’s target value is achieved, the obligated reserve’s value should track with the 3-year averaged operating budget.

Unrestricted Funds

Unrestricted funds are monies that are available for AFS to spend. Unrestricted funds may come from excess revenue or contributions that are not constrained by donor requests. Unrestricted funds are managed by the investment advisor as part of the investment fund, with the remainder comprising AFS’ net balance of assets and liabilities. These assets and liabilities are less liquid and include fixed assets, receivables, and prepaid payments, less liabilities.

Restricted Funds

Restricted funds are monies that are constrained either by donor request or by the contributing entity or were established by the Governing Board. Contributing entities include AFS Chapters, Sections, Divisions, and programs that have entrusted funds to AFS for investment. These funds are managed by the investment advisor as part of the investment fund. Each fund shall adhere to the contributor’s intentions and define a spending plan, investment approach, and procedures over fund administration. The ED shall provide at least semiannual reports to unit treasurers by January and July of each year.

The following programs have monies in the restricted funds portion of the investment fund:

The Carl R. Sullivan Fisheries Conservation Award Fund supports the annual purchase of the “Sully” award.

The Carl R. Sullivan International Endowment and Developing Countries Fund encourages international fisheries activities that support the Society’s and the International Fisheries Section’s long-term international goals.

The J. Frances Allen Scholarship Fund provides at least one $2,500 scholarship annually to a deserving woman doctoral candidate.

The William R. Mote Fund shall be managed with the goal of being a perpetual award that appreciates from investment gains and additional donations.

The Past Presidents Endowment Fund promotes networking of fisheries professionals throughout the world, particularly younger members, students, emerging leaders, underrepresented minorities, professionals in developing nations, and those who bridge nations and cultures.

The Publications Endowment Fund, established in 1987, supports the publication of AFS and unit publications for which outside support is lacking. The Publications Endowment Fund was funded via a $1 fee on books published before 1987 and a $2 fee on each book sold for those published after 1987. That charge has since been terminated.

The Shelby Gerking Continuing Education Program Fund increases opportunities for professional development for fisheries professionals.

The Skinner Memorial Fund provides travel scholarships for students to attend an AFS Annual Meeting.

The Snieszko Fund was initially funded by Stanislaus and Julia Snieszko for the benefit of the Fish Health Section. It funds the S.F. Snieszko Distinguished Service Award as well as student travel and best student paper awards.

The Steven Berkeley Fellowship Fund supports the Marine Fisheries Section’s Steven Berkeley Marine Conservation Fellowship.

Management of unit funds is determined by the units. Units periodically request funds to be used to achieve their individual program missions.

Short-Term Money/Bank Credit Line

The ED is responsible for managing short-term money. The amount in this category of funds varies annually and seasonally because AFS revenue is seasonal and concentrated in the November–January time frame (annual dues payment period) and in the months prior to the Annual Meeting when registration funds can be substantial, whereas AFS operational expenses are more evenly spread throughout the year. This operating cash must be liquid and not subject to significant market (interest rate/duration) risk or credit quality risk.

Short-term money is required to cover liabilities that may arise for prepaid orders, subscriptions, and employee benefits. The types of securities authorized for short-term money include bank accounts (checking, savings, money markets), time deposit accounts (CDs, U.S. Treasury bills and other short-term government paper, commercial paper, and other cash equivalents with an average rating of AA). The ED shall review the operating cash projections and prepare a schedule of investment fund deposits or withdrawals in advance of each quarterly FPPC meeting. Transfer of money from the investment fund to short-term money shall be made only on authorization by the ED. Whenever there appears to be more than a nominal amount above projected requirements in short-term money, the excess shall be transferred to the obligated reserve fund if money can be transferred efficiently. If monies cannot be moved efficiently between the obligated reserve or unrestricted reserve and the short-term money account, then the funds should remain in the short-term money account.

Bank credit line is a financial lending instrument and source of short-term resources when Society cash flow is low. The revolving credit line charges a floating rate of Prime + 1% and interest is paid monthly on borrowings. The principal may be paid off at any time and must be fully paid off for a minimum of 30 days each year. The Deputy Director and Executive Director are authorized to request advances and authorize repayments. The bank may demand payment on this note at any time. The note is secured by a collateral account and some or all of the collateral may be released in the future contingent on AFS’s financial condition improving.

Financial and Investment Objectives

The financial objective of the investment fund is to attain an average annual real total return (net of investment management fees) equal to that of a moderately aggressive benchmark with lower overall risk.

Investment Management Structure

The ED, with the advice of the FPPC, is authorized to delegate investment fund management to an investment advisor, who is given discretionary powers under the guidelines provided in this policy and supplemented by instructions from the FPPC. The investment manager shall be appointed by the President and Executive Director with the advice of the FPPC.

The FPPC shall report the performance of the investment fund quarterly to the Management Committee.

Portfolio Composition and Asset Allocation

To achieve its objectives, the investment fund shall be divided into equity and fixed-income components and shall be diversified both by asset class and within asset classes (e.g., within equities by economic sector, industry, quality, and size and among different sectors of the fixed income market). The purpose of such diversification is to provide reasonable assurance that no single security, class of securities, or specific investment style will have a disproportionate impact on the investment fund’s aggregate results.

The purpose of the equity component is to provide a total return that will provide for growth in principal and current income to support any desired spending requirements while increasing the purchasing power of the investment fund. The American Fisheries Society recognizes that the pursuit of these long-term objectives entails the assumption of market variability and risk. Equities should normally represent approximately 70–80% of the total investment fund assets at market value. Although the actual percentage weighting in the equity component will vary with market conditions, asset allocation will be closely monitored whenever levels exceed 80% or fall below 70%. Should the allocation move outside of these ranges, additional funds will be transferred as needed to bring the overall asset mix back within the policy range.

The purpose of the fixed income component is to reduce the overall volatility of the investment fund returns and to provide a hedge against the effects of a prolonged economic contraction. The fixed income component should normally represent 20–30% of the total investment fund assets at market value, although the actual percentage will fluctuate with market conditions. Should the allocation move below 20% or above 30%, funds will be transferred as needed to bring the overall asset mix back within the policy range.

Additions to principal will be allocated to the investment manager by the FPPC (through the ED) following the general rule that new cash will be used to rebalance the investment fund in the direction of the 70–80%/20–30% equity/fixed-income ratio. Rebalancing will be completed periodically in response to market and investment fund conditions.

Performance Objectives

In addition to the overall objective of a real return of 5% annually over a five-year rolling period, the following performance objectives (net of fees) are expected to be met by the fund and its individual components.

The performance objective for the equity portion of the investment fund is to perform similarly to a moderately aggressive benchmark selected by the investment advisor, or to appropriate sector benchmarks. The performance objective of the fixed income component is to outperform the Barclays Capital Aggregate Bond Index or another benchmark appropriate for fixed-income investments.

Risk Tolerance

Risks taken should generally be limited to those expected from market fluctuation in the form of assets employed and ideally be lower than the tracking benchmark. The investment advisor maintains a moderately aggressive management approach to managing the investment fund.

Monitoring of Objectives and Results

The FPPC shall quarterly review investment fund performance with the investment advisor to ensure that performance expectations remain in place.

All objectives and policies are in effect until modified by the Management Committee. If at any time, a member of the Governing Board, Management Committee, or FPPC; ED; or investment advisor believes that an established policy or guideline inhibits the performance of the investment fund, it is that individual’s responsibility to clearly communicate this view to the FPPC chair, AFS President, and ED.

Goal: To position the American Fisheries Society for launching a planned giving initiative for the future of the Society.

Process:

To remind Society members of the importance of making a will,

To introduce the idea of making a planned gift to the Society,

To identify a group of AFS members who might make a bequest to AFS, and

To continue to cultivate any interest expressed or commitment made by members to remember AFS in their will.

Action Plan:

Identify a member group to spearhead this effort. The Past Presidents’ Advisory Council (PPAC) is committed to lead this effort with support from AFS staff.

Identify previous and future planned gifts. Prepare a list of donors who have made a planned gift to AFS in the past. Also prepare a list of those members who have notified AFS of their intention to make a planned gift.

Identify prospects. Review all donor files for planned giving prospects; examples are 30-year and 40-year members, Golden Members, Life Members, Past Presidents, and donors of large gifts. Compile a list of prospects and provide this list to the Past Presidents’ Advisory Council for their review and additions.

Identify for each possible donor a personal member contact who will spearhead the effort personally.

Write an article on planned giving. In 1989, AFS Executive Director Carl Sullivan wrote a nice article for Fisheries on bequests to AFS. A similar article should be prepared as a kickoff event to the planned giving program. It could be presented under the name of the chair of the Past Presidents’ Advisory Council or the key person spearheading the planned giving effort for the PPAC. When published, there should be a response card included in Fisheries for the convenience of members who wish to respond or seek additional information. Reprints of the article should be distributed at AFS Annual Meetings, unit events, symposia, AFS trade shows and similar gatherings of members.

Create a bequest recognition group. This concept will be introduced in the Fisheries article on planned giving. Past Presidents, officers, and/or Governing Board Members could be invited to join as charter members of this group; this group may be helpful in identifying, evaluating, and cultivating prospective donors.

Design a brochure with tear-off reply card. This brochure would be included in the first mailing to prospects after the appearance of the article on bequests in Fisheries; this brochure could accompany reprints of the article in future distributions.

Develop letters and enclosures for use in mailings to prospects:

Prepare letters on AFS letterhead from the chair of the Past Presidents’ Advisory Council or the key person spearheading the planned giving effort for the PPAC to introduce the program and to encourage members to request more information.

Prepare an enclosure such as a reply card upon which the member may insert their name, address, and telephone and check off appropriate boxes to indicate interest, to request information, or to make a commitment.

Enclose a confidential, postage-paid reply envelope in mailings.

Create a thank-you letter when a planned gift is made; acknowledge the gift in the AFS annual report, with permission of donor.

Create a follow-up letter when no response has been obtained by a certain date.

Create ads on planned giving. These should be small, bold ads for insertion in Fisheries to encourage members to remember AFS in their will.

Schedule an annual mailing. This mailing of planned giving materials should coincide with a brief ad or a promotional article in Fisheries.

Monitor results. The AFS staff and the Past Presidents’ Advisory Council will monitor results to determine appropriate follow up with prospects (information response, personal visits by volunteers, and other forms of interaction).

Maintain contact with bequest donors. The Past Presidents’ Advisory Council and AFS staff will stay in touch with bequest donors, continuing to provide them with information on AFS so that the donor is made to feel appreciated and valued for their commitment.

Result: The Society will have identified, approached, and cultivated those members most likely to be interested in making a planned gift to the Society and will have uncovered future sources of revenue. This effort also may result in more life income gifts from the targeted group of AFS members.

Purpose: New Initiatives are strategic projects that enhance member and unit services while advancing the major goals and mission of AFS. These projects may be one-time activities or may entail the creation of new services and activities that later become routine operations (e.g., leadership development grants, new journals).

Background: In 2005, the Enhancement of AFS Value Committee was appointed to develop recommendations for AFS services and activities that could be accomplished under the increased financial security of AFS. Under the guidance of the committee, the AFS Governing Board identified services and activities to enhance member services, aquatic stewardship, and information transfer and outreach. Three projects were selected for further pursuit:

The development of an open-access, electronic journal dedicated to marine and coastal fisheries,

The support of AFS leadership development (through a grant for Governing Board members’ travel to the Mid-Year Meeting), and

The enhancement of public outreach by expanding the scope of AFS staff (through the hiring of a policy and public outreach coordinator in Bethesda).

These initiatives have now become routine operations and will not be affected by subsequent considerations of new initiatives.

General Overview: New initiatives are focused on either membership services or unit services but share the strategic goal of maintaining and enhancing AFS relevancy. Initiatives are identified from a variety of sources; some initiatives may generate funds, some will be revenue neutral, and some will entail continued costs. The Executive Director in concurrence with the AFS Officers will identify the total amount of funds available to support each type of new initiative (i.e., funds available to support new unit services/activities and total funds available to support new membership services/activities).

Unit Services: Initiatives for unit services provide seed money for activities or services to assist units in reaching their strategic goals and in carrying out their business. Seed money will be returned to AFS after a period of time not less than one year but not to exceed three years after completion of the project or activity. Requests for funds to support meetings should adhere to the AFS policy on Support for Meetings (Section 12.11, under Section 12, Operational Policies and Procedures).

Membership Services: Ideas for initiatives for membership services may come from various sources, including focus groups, membership surveys, units, individual members, and AFS staff. These needs should be activities or services that are not available elsewhere. Providing services to meet these needs becomes an investment in our future, with the desired outcome being the retention and recruitment of early career professionals and students to AFS and maintaining our relevancy as a professional association.

Operational Guidelines, Unit Services:

The purpose of this section is to establish guidelines for the identification, selection, and implementation of new initiatives to support unit services.

Application Submission Process: The Executive Director will send the application and guidelines for preparation and submission of applications to unit Presidents (Division presidents may forward material to Chapter presidents). The Executive Director will also suggest an upper limit for individual requests.

Successful applications will include a brief narrative describing the strategic goal of the initiative, the need for the initiative, how the success of the initiative will be measured, the amount requested, and a description of how and when funds will be generated to return the seed money. Units submitting single requests that encompass multiple tasks will be asked to prioritize tasks in the event that a full request cannot be granted.

To ensure equal consideration, applications will be due January 5 (or the first business day after January 5), with funding outcome to be determined no later than February 15. This will avoid units seeking funds for the same initiative at the mid-year Governing Board meeting (in the form of a motion with budget implications).

Completed applications will be submitted electronically to the President with copies to the Executive Director on January 5.

Selection Criteria: The Governing Board will screen the applications and make the awards; late applications will not be considered. The screening process is general, seeking to ensure that seed monies will be repaid and that the activities proposed are consistent with the AFS mission. Screening and Governing Board voting may occur electronically. Applications approved for funding will be those that make a strong case for the unit’s ability to recover funds. All approved applications will be funded. However, if the total funds requested across units exceed that available, then approved awards will be funded to ensure representation across Divisions and among Sections and to facilitate funding of initiatives from units that have not received prior funding.

Reporting Requirements: Units funded through this process are required to submit progress reports to the Governing Board in time for the mid-year and annual meetings of the Board. Progress reports should be brief and include a statement on outcomes, challenges, and progress towards returning funds.

A list of funded initiatives will be posted to the AFS website by AFS staff.

Operational Guidelines, Membership Services:

The purpose of this section is to establish guidelines for the identification, selection, and implementation of new initiatives to support membership services. In general, the Executive Director develops business plans for 3-5 initiatives deemed to be of highest priority, and the Governing Board selects initiatives to pursue, depending on costs and other factors.

Ideas for initiatives to support membership services may come from various sources, including membership surveys and focus groups (these ideas would be identified in reports of the committees responsible for such surveys), AFS units, individual members, and AFS staff. The Management committee will have access to reports and findings of survey committees and may elect to propose ideas from these sources.

Proposal Submission Process: In early October, the Executive Director sends a call for proposal for new initiatives to support membership services to the Governing Board, the general membership, and AFS staff. The call includes guidelines and deadlines for submission (January 5). Guidelines for proposing new initiatives for membership services are established by the Governing Board.

Selection Criteria: The Governing Board in concurrence with the Executive Director will select no more than five initiatives for further consideration. Selection may be accomplished through e-mail voting, with each voting member of the Board selecting (and ranking) their top three priorities. Criteria for selection include (1) alignment with strategic goals and mission of the AFS, (2) cost considerations, and (3) ability to evaluate success of the outcome. Higher priority may be placed on initiatives that address the retention and recruitment of early career professionals and students to AFS and those that focus on maintaining our relevancy as a professional association. The Board votes are tallied, and the overall top five candidates are selected for business plan development. The outcome will be communicated to the Governing Board at the Mid-Year Meeting.

The Executive Director, working with the originator(s) of the proposals, will develop business plans for selected initiatives and present the plans to the Governing Board at the following mid-year meeting. Typically, business plans will require six months to one year to develop.

At the Mid-Year Meeting, the Governing Board will review the business plans and, as warranted, select initiatives to support based on available funds. Business plans for new initiatives should be examined in light of the long-term financial status of AFS. The Governing Board may elect to partially fund an initiative if existing funds are insufficient (e.g., an initiative may require two or three years of funding to be fully funded). In the case of initiatives requiring more than one year of funding, the Executive Director will include budget costs for two or more years in the proposed AFS budget. To ensure the financial well-being of AFS, it is desirable to select at least one new initiative that will generate revenue (rather than being revenue-neutral or revenue-negative). Unfunded initiatives may be resubmitted in later years for consideration.

The American Fisheries Society (AFS) disaster relief will focus on professional needs of Society members. Other agencies and institutions have responsibility for humanitarian needs. This does not mean that AFS is not sensitive to personal needs of members. To the contrary, addressing professional need is fundamental to addressing human need because during times of disaster, professional capacity is critical to restoring order and generating outreach in communities as well as generating/reestablishing definition in the lives of individual persons.

The organizational structure of AFS will be utilized in disaster response. The president of the AFS Division within which the disaster occurs will have the principal leadership role in terms of (1) recommending to the Society President that disaster be declared and (2) activating and directing disaster relief within the Division. Tasks can be assigned by the Division president, but the Division president has ultimate authority and responsibility. Chapter communications to the Division president will come through the Chapter president or a person designated by the Chapter president unless the Chapter president has been impacted by the disaster to the extent that they cannot function in this capacity. In such a case, the Division president, in consultation with the Society President, will appoint a Chapter contact person (preferably from the Chapter membership).

Operations

The most important activity immediately following the disaster is to locate AFS members in the impacted area. This is essential in order to keep them connected and in communication with the professional support system provided by the AFS. This initial contact will clearly communicate what AFS services are available and how they can be obtained. It will also provide each member with the contact information for their Chapter President or other designated disaster relief coordinator for the Chapter.

For this activity to function, it is essential that membership rosters be kept up to date in the Chapter, Division, and Society records. These records should include persons who hold Society and Chapter memberships, those who hold only Society memberships, and those who hold only Chapter memberships. Without up-to date-rosters, there can be no certainty that all members have been accounted for following a disaster.

Displaced members should make every effort to contact their Chapter president. If this cannot be done, then displaced members should contact the Society Office. The Society headquarters will then contact the Division president, who in turn will contact the Chapter president or other designated contact for the Chapter.

Establish a centralized distribution and control center outside of the impacted area. This center will serve as the operational hub for communications and for the coordination of relief activities, including identification of need and availability of materials. This center will be staffed by one paid coordinator, selected by the Division president and approved by Division officers. The coordinator’s job is to maintain operations, communications, and records for disaster relief. The coordinator will report directly to the Division president. It is the responsibility of the Division president to determine the flow of communication between coordinator, Chapters, and Division.

The Society, through the Division, should be prepared to employ the coordinator up to two years following the disaster.

It should be noted that the coordinator could handle multiple disasters in the same Division should it be necessary to do so. However, if there should be a new disaster in a different Division, it is recommended that a new coordinator be hired, if AFS is financially able to do so.

Establish a relief disbursement center on the edge of the impacted area. This enables relief supplies from outside the impacted area to get to (not in) the area. Although persons from outside the impacted area may have good intentions regarding disbursement of relief supplies, they can encounter local challenges due to their unfamiliarity with the area and current situation. It is best for AFS members staffing the relief disbursement center to take responsibility for transport and disbursement of relief supplies into the impacted area. The relief disbursement center is staffed by volunteers, not paid staff. However, the coordinator will coordinate donated items from the donor(s) to the relief disbursement center and from the center to the intended recipient(s).

Fiscal Responsibilities of Disaster Relief

All financial donations toward disaster relief will be made to the Society Disaster Relief Donation Fund. Any donations received by the affected Division will be forwarded to the Society Disaster Relief Donation Fund. The Society will periodically update the affected Division on donations that have been received in order for the affected Division to make best use of the monies.

The affected Division will set up a separate bank account to address disaster relief and will be the sole distributor of the Division’s disaster relief distribution funds to affected AFS members. The Division treasurer will manage the distribution of monies as well as maintain and manage the account. The Division executive committee or an individual or group appointed by the Division president will prepare a budget for anticipated distribution of funds. As needed, the Division will request transfer of funds from the Society Disaster Relief Donation Fund to the Division. The affected Division will be responsible for providing the Society Governing Board and the AFS Executive Director with financial statements (income/expenses/balance) periodically and upon request. When preparing its annual income tax return, the Division must account for funds received from the Society Disaster Relief Donation Fund as well as expenses to the Division’s disaster relief distribution account because these actions are Division functions.

Response Framework

The AFS Disaster Relief Website will be maintained on the Division website for the affected area with a link from the Society website.

The Society will hold in reserve a designated amount for disaster relief.

Immediately Following an Event:

The Division president will immediately contact the Chapter president(s) in the impacted area. The Chapter president(s) will make recommendations to the Division president regarding an AFS declaration of disaster. If the Chapter president(s) cannot be contacted, the Division president will contact another elected Chapter representative.

The Chapter president(s) or other designated Chapter representative(s) will immediately begin locating members in their respective Chapter(s) and checking off members using current rosters. These checkoffs will be forwarded periodically to the Division president, who in turn will forward them to the Society Office. Additionally, the Chapter president(s) will collaborate with the Society headquarters to identify and locate Society members in the region who are not Chapter members.

The Division president will immediately contact the Society president and request (1) a disaster declaration, (2) permission to establish a distribution and control center, (3) permission to seek and hire a coordinator for the distribution and control center, and (4) the release of one-third of the Society’s budgeted disaster relief funds to the Division.

The Society President will call an emergency meeting of Society officers and the AFS Executive Director to determine if a disaster declaration is warranted and, if so, will request approval to release disaster relief funds, establish a distribution and control center, and hire a coordinator for the center.

Following these actions by the Society officers, the Society Governing Board will be notified.

Following a declaration of disaster by the Society President, the Division president will establish liaison with the impacted Chapter(s) via the respective Chapter president(s) or designated Chapter representative to identify immediate professional needs of impacted AFS members and authorize the Division treasurer to establish an independent account for the Division’s disaster relief distribution funds.

Recommended Outreach Schedule:

Within two weeks of the disaster: the Society and Division disaster relief funding mechanisms will be in place.

Within two weeks of the disaster: all AFS Society members will receive notification that disaster relief has been activated and provided information regarding mechanisms for disaster relief donations.

Within two months of the disaster: the distribution and control center will be staffed and operational.

Within two months of the disaster: all impacted AFS members will be individually identified, located, and if possible, contacted by their Chapter representative(s) to advise them of relief support coming from AFS (i.e., complimentary memberships, subscriptions, availability of scholarships to AFS meetings, and the Division’s disaster relief distribution and control center).

Within six months of the disaster: impacted AFS members receiving scholarships to AFS Meetings will be notified of their awards.

Subject to the availability of funds (e.g., corporate sponsors, donations), AFS should consider awarding grants to members and their affiliated institutions in the impacted region to help support completion of thesis and dissertation projects impacted by the disaster.

Reference

Heitman, J. F., D. C. Jackson, D. Pender, and R. L. Curry. 2008. Development and implementation of the American Fisheries Society Disaster Relief Program. Pages 169–183 in K. D. Mclaughlin, editor. Mitigating impacts of natural hazards on fishery ecosystems. American Fisheries Society, Symposium 64, Bethesda, Maryland.

Memorandum of Understanding between the Fisheries Conservation Foundation and the American Fisheries Society

I. Purpose

The Memorandum of Understanding (MOU) is made and entered between the Fisheries Conservation Foundation (FCF) and the American Fisheries Society (AFS). Both signatories of this MOU are referred to as “Partners.”

The purpose of this MOU is to designate a collaborative relationship between FCF and AFS in which the partners assist each other in carrying out their respective missions.

II. Background

FCF, founded in 2003, is a science-based conservation-oriented foundation representing fisheries scientists. FCF promotes public awareness of fisheries resource issues and relevant scientific research, as well as the enlightened management of fisheries resources for their optimum use and enjoyment by the public.

AFS, founded in 1870, is the oldest and largest professional society in the world representing fisheries and aquatic scientists. AFS seeks to improve the conservation and sustainability of fishery resources and aquatic ecosystems by advancing fisheries and aquatic sciences and promoting the development of fisheries professionals.

III. Mutual Benefits

It is mutually beneficial for FCF and AFS to work together to

Increase scientific knowledge on important fisheries resource issues;

Communicate science-based information to relevant decision makers;

Increase public awareness of fisheries resource conservation issues;

Identify strategies to assure that resource management is based on sound science;

Develop support to help implement such strategies among relevant constituencies and the general public.

IV. Responsibilities

FCF and AFS will together work to:

Encourage fisheries scientists and managers to conduct new education/outreach programs designed to distribute scientific findings to decision makers and the public.

Organize meetings, workshops, and other events for scientists, nongovernmental organizations, resources managers, and policy makers to develop plans and policy considerations for fisheries resource conservation efforts.

Develop tools to communicate relevant scientific information to decision makers and the public.

Develop and market strategic proposals for funding from individuals, private foundations, government agencies, and other sources to support collaborative work.

It is mutually agreed and understood by the partners that

This MOU is neither a fiscal nor a funding obligation document.

It shall be the goal of both parties to ensure joint organizational recognition (e.g., logos, URLs) on relevant public events/products produced as joint efforts under this MOU.

Each signatory party shall obtain prior approval from the other for all joint press releases, advertisements, or other statements regarding projects or work products specified under this MOU and intended for the media, relevant decision makers, or the public. Each party need not obtain such prior approval for any activity conducted solely and independently.

The Partners shall consult regularly to discuss actions to implement the purpose of this MOU.

V. Terms of Agreement

This agreement shall be reviewed by both partners annually to determine whether it should be continued, modified, or terminated. This agreement shall have no specified term limitation but may be terminated by either party upon 30 days written notice.

VI. Principal Contacts:

The principal contacts for this agreement are

Julie Claussen, Executive Director

Fisheries Conservation Foundation

1816 South Oak Street

Champaign, IL 61820

(301) 897-8616 (x208) Phone

(301) 897-8096 Fax

[[email protected]]

___________________

Dr. Doug Austen, Executive Director

American Fisheries Society

5410 Grosvenor Lane, Ste. 110

Bethesda, MD 20814

(301) 897-8616 Phone

(301) 897-8096 Fax [email protected]